Since opening an office in Mauritius in 2020 to coordinate MOL’s marine environment restoration and social contribution activities, MOL has also examined how the Mauritius jurisdiction can be used to support regional investment activity in Africa.

A July 2025 meeting between former MOL CEO Mr Takashi Hashimoto and Mauritius Prime Minister Dr Navin Ramgoolam during which the potential of Mauritius as a gateway for East Africa was discussed

A July 2025 meeting between former MOL CEO Mr Takashi Hashimoto and Mauritius Prime Minister Dr Navin Ramgoolam during which the potential of Mauritius as a gateway for East Africa was discussed

Although strict Japanese Controlled Foreign Company (J-CFC) or Anti-Tax Haven rules and the absence of a Double Taxation Avoidance Agreement (DTAA) combine to eliminate any tax advantage offered by the Mauritius jurisdiction, the current war in the Middle East is bringing renewed interest in Mauritius as a potential hub for regional investment activity in Africa.

This blog post seeks to shine a light on the complex J-CFC rules that apply to Japanese companies seeking to use “low tax” or “tax competitive” jurisdictions such as Mauritius. It is hoped that a better understanding of the heightened substance and main business test criteria under J-CFC rules will aid Mauritius IFC stakeholders and Japanese companies looking to expand the use of the Mauritius jurisdiction by Japanese companies for regional trade and investment activities. A key insight is that despite the strict J-CFC rules or Anti-Tax Haven rules, a Japanese company possessing the strategic clarity to use Mauritius for regional investments and intent to establish sufficient substance and management control can ultimately derive a tax advantage while remaining in compliance with these rules.

The Mauritius IFC

Over the past three decades, Mauritius has transformed into a well-established international financial centre (IFC), offering political and legal stability, investor-friendly regulation, and tax efficiency.

Having first emerged as a preferred jurisdiction for routing investments into India – between 2000 and 2017 Mauritius was the largest source of Foreign Direct Investment into India accounting for 34% - today Mauritius is positioned as a gateway for investments into Africa, increasingly favoured by international development finance institutions, private equity and fund managers.

The Mauritius IFC offers investor in Africa several key advantages including (but not limited to):

-

Political Stability, Economic Stability and legal Certainty

- Stable “Westminster style” full democracy

- Robust legal & legislative system, with the highest Court of Appeal at the UK Privy Council

- Investment-grade credit rating (Moody’s Baa3).

-

Trusted Jurisdiction of International Repute

- Fully compliant with OECD, EU and FATF standards

- Trusted jurisdiction for fund domiciliation and cross-border structuring

-

Strategic Gateway and cross-border investment hub for Africa

- Regional economic bloc integration (members of SADC and COMESA RECs, AfCFTA signatory).

- Convenient time zone bridging Asia and Africa (same time zone as Dubai).

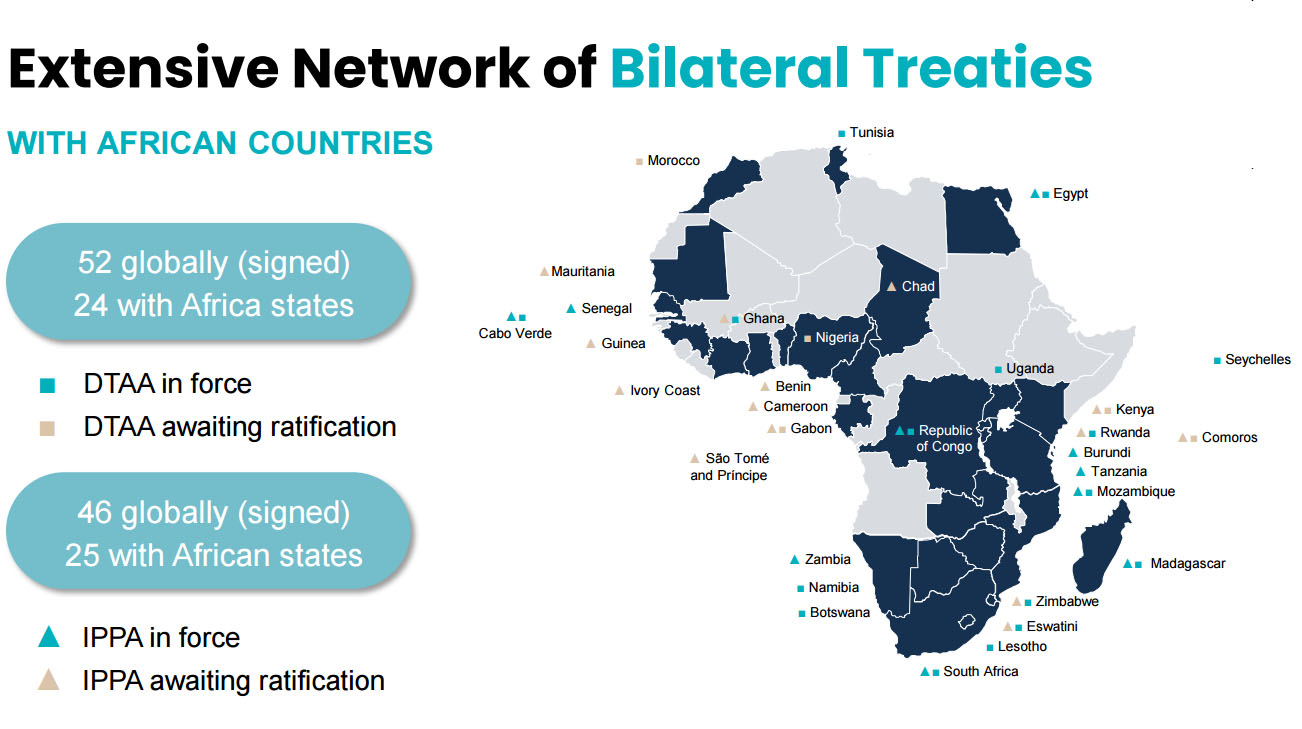

- Tax Mitigation through 52 Double Taxation Avoidance Agreements (DTAA), of which 24 in Africa

- Risk Mitigation through 46 Investment Promotion and Protection Agreements (IPPA), of which 25 in Africa

- No foreign exchange controls

-

Tax Efficiency

- 15% corporate tax with 80% exemption on qualifying foreign income (effective rate c.3%).

- No capital gains tax, no dividend or withholding tax, no share transfer tax

- 15% flat personal income tax and no inheritance tax.

-

Business Friendly Environment

- Ranked 13th globally (1st in Africa) in World Bank’s Doing Business Index 2020.

- Strong financial services, banking and capital markets sectors

- Efficient company incorporation, licensing, and regulatory processes.

- Bilingual (English/French) Human Capital at reasonable cost

- Availability of well qualified professionals (especially accounting and legal)

Mauritius’ network of IPPA and DTAA bilateral treaties in Africa (Source: Intercontinental Trust Limited Jan 2026)

Mauritius’ network of IPPA and DTAA bilateral treaties in Africa (Source: Intercontinental Trust Limited Jan 2026)

The Mauritius IFC & Japan

Despite Mauritius’ distinct and cumulative advantages, there remains a notable lack of Japanese companies operating in Mauritius. While Mauritius’s comparatively small market size and lack of natural resources partly explains why Japanese exporters and trading houses over-look Mauritius, this does not explain why so few Japanese companies use the Mauritius IFC to route regional investments in Africa.

As stated above, the absence of Investment Promotion Protection Agreement (IPPA) and Double Taxation Avoidance (DTA) agreements between Japan and Mauritius certainly has an impact, and MOL strongly supports the ongoing discussions between the Governments of Japan and Mauritius to expedite the establishment of these key agreements in the coming years.

August 2025 meeting between then Japanese Prime Minister Shigeru Ishiba and Mauritius Prime Minister Dr Navin Ramgoolam during which an agreement was made to sign an IPPA between the two countries in advance of a DTAA.

August 2025 meeting between then Japanese Prime Minister Shigeru Ishiba and Mauritius Prime Minister Dr Navin Ramgoolam during which an agreement was made to sign an IPPA between the two countries in advance of a DTAA.

But what may also be missing – especially on the side of Mauritius IFC stakeholders promoting the tax advantages of the Mauritius jurisdiction to Japanese companies - is an insight into the complex and diluting effects of the J-CFC / Anti-Tax Haven rules, and the heightened test thresholds that Japanese companies considering to use the Mauritius IFC must comply with in order to secure a tax advantage.

Japan’s Controlled Foreign Company (CFC) or Anti-Tax Haven Rules

J-CFC rules are intended to prevent tax base erosion by Japanese corporations establishing subsidiaries (and accumulating profit) in low tax countries. Under these rules, income earned by an affiliate company in a low tax jurisdiction (Foreign Related Company or “FRC”) may be aggregated (i.e. included) in the Japanese parent company’s taxable income and thus subject to Japanese effective tax rates. In other words, the “low tax” or “tax competitive” advantages offered by the Mauritius IFC are not automatically available to a Japanese company using a Mauritius FRC.

J-CFC rules apply, and a Mauritius FRC’s total income may be aggregated in the Japanese parent company’s taxable income, if one or more of the following conditions apply:

- Japanese resident shareholders own more than 50% of the FRC (including indirectly via intermediate holdings in third countries);

- Japanese residents hold de facto control over the FRC (even without owning more than 50% of FRC);

- The FRC is classified under J-CFC rule as a Paper Company;

- The FRC is not classified under J-CFC rules as a Paper Company but also does not satisfy all the J-CFC rules Economic Activity Tests;

- The effective tax rate of the FRC is less than 20% (30% in the case of a Paper Company)

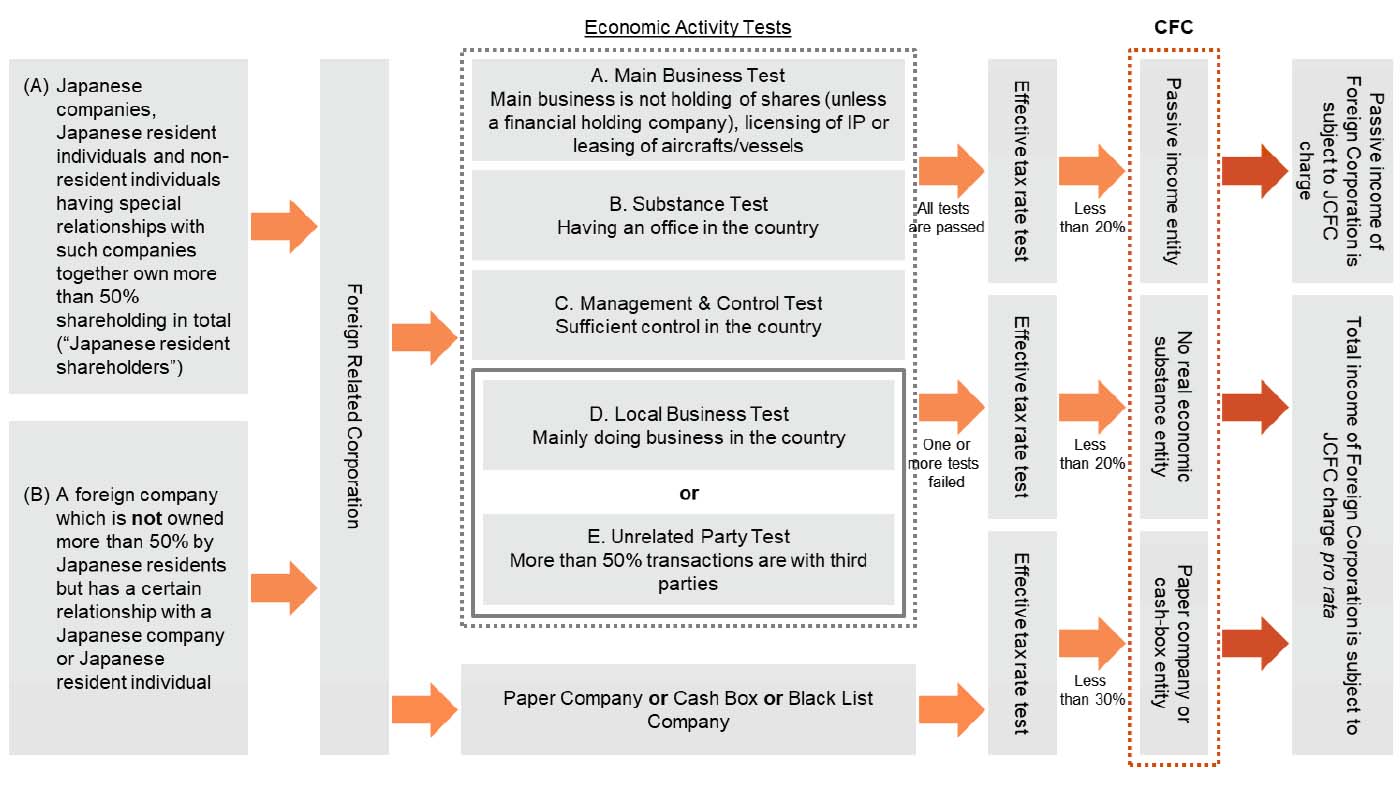

J-CFC / Anti-Tax Haven rule decision tree guide (NB: other conditions and exemptions may apply which are not shown in this decision tree)

J-CFC / Anti-Tax Haven rule decision tree guide (NB: other conditions and exemptions may apply which are not shown in this decision tree)

As Mauritius’ headline corporate tax rate is 15%, and which for foreign income can typically be further reduced via partial exemptions to an effective rate of c.3%, a Mauritius FRC of a Japanese company will invariable be deemed “low-taxed” and therefore subject to J-CFC rules. Without satisfying all the various Economic Activity Tests laid out under the J-CFC rules, the income of the Mauritius FRC will be aggregated in the Japanese parent company’s taxable income and subject to Japanese effective tax rates, which for larger companies exceeds 30%. This treatment applies even if no dividends are distributed by the Mauritius FRC (i.e. profits retained outside Japan in the Mauritius FRC cannot escape taxation in Japan).

Whilst tax is unlikely to be the only consideration, it remains a vitally important one in decision making and the inability of a Japanese company to secure a tax advantage by using a Mauritius FRC is clearly detrimental when seeking to promote use of the Mauritius IFC to Japanese companies.

So, what steps can Japanese companies take to be able to use a Mauritius FRC and secure a tax advantage?

Step 1: Mauritius FRC must not be classified as “Paper Company” under J-CFC rules

The total income of a FRC classified as Paper Company is automatically (with certain exceptions not detailed here) subject to aggregation in the Japanese parent company’s taxable income and subject to Japanese effective tax rates.

A “Paper Company” is defined under J-CFC rules as an FRC which fails to meet both of the following conditions

- FRC maintains a fixed place of business necessary to conduct its main business; and

- FRC functions with its own administration, control and management in the country where its head office is located

Furthermore, in seeking to satisfy both conditions, an FRC must also pass a) Substance, and b) Management and Control tests

- Substance Test: The fixed place of business is necessary for the conduct of the FRC’s main business and employees conduct business at the fixed place of business

- Management & Control: The FRC has a full-time Director and employee responsible for the formulation and outcomes of business policies, performance goals and business plans. Shareholder and Board meetings should also be held in (chaired from) Mauritius, and accounting books should also be prepared and held in Mauritius.

A Mauritius FRC satisfying substance and management and control tests above and not classified as a “Paper Company” can qualify to benefit from Mauritius’s tax advantages provided it also passes the J-CFC rules Economic Activity Test.

Step 2: Mauritius must FRC pass the Economic Activity Test under J-CFC Rules

The J-CFC rules Economic Activity Test actually comprises four separate tests, each of which must be satisfied for the Mauritius FRC to pass the Economic Activity Test.

The four separate tests are:

- Main Business Test;

- Substance Test;

- Management and Control Test; and

- Local Business and Unrelated Party Test

In complying Step 1 Mauritius FRC must not be classified as “Paper Company” above, a Mauritius FRC will already satisfy the 2) Substance and 3) Management and Control Tests.

The 1) Main Business Test is almost certainly the highest hurdle to clear for Japanese companies looking to establish a Mauritius FRC for regional investments. This is because the basic activity of “holding shares or financial securities” – a common first step for investors structuring investments in Mauritius - is specifically excluded as a permitted activity under the Main Business Test. Certain other specified businesses activities including the licensing of intellectual property rights and copyrights, and certain aircraft and ship leasing structures, are also specifically excluded. Highlighting the complexity of J-CFC rules and their application, certain exemptions apply to these excluded specified business activities!

The 4) Local Business and Unrelated Party Test requires that a Mauritius FRC also undertakes its main business activity mainly in Mauritius, except that for certain specified main business activities including wholesale trading, financial services, air transport and ocean transport, the Mauritius FRC must instead satisfy an Unrelated Party Test based on the ratio of unrelated party transactions to total transactions.

J-CFC Rules Economic Activity Tests

If the Mauritius FRC cannot satisfy each of the four separate tests, the Mauritius FRC will be deemed to possess “no real economic substance”, and the total income of the Mauritius FRC will be subject (with certain exceptions not detailed here) to aggregation in the Japanese parent company’s taxable income and subject to Japanese effective tax rates

On the other hand, if the Mauritius FRC does satisfy all four separate tests, the Mauritius FRC will be approved as a “Passive Income Entity” and only certain passive income of the Mauritius FRC (certain dividends, certain interest income, certain capital gains, etc.) will be subject to aggregation in the Japanese parent company’s taxable income. Furthermore, the active business profits of the Mauritius FRC will not be subject to aggregation.

“Regional HQ” Main Business Test exemption

As suggested above, the J-CFC’s specified exclusion of the basic activity of “holding shares or other securities” as a main business activity of a Mauritius FRC under the 1. Main Business Test is likely to be the highest hurdle to clear for a Japanese company considering a Mauritius FRC for the first time.

However, the J-CFC rules also provide an exemption to the Main Business Test for a “Regional HQ” strategy, in which a Mauritius FRC is strategically positioned to satisfy all of the following criteria:

- A Japanese company owns, directly or indirectly, 100% of the share capital of the Regional HQ FRC;

- Regional HQ FRC has physical presence and employees conduct the supervising operations;

- Regional HQ FRC has 2 or more subsidiaries where the Regional HQ FRC owns 25% or more of the issued share capital directly (Controlled Companies);

- More than 50% of a Controlled Company's share capital is owned by the Japanese parent group including Regional HQ / FRC, etc.

This Regional HQ strategy exemption suggests that in addition to assessing the merits of a Mauritius FRC for a specific regional investment transaction (which may fail the main business test), Japanese companies should also consider the tax merits of a broader strategy to establish a Mauritius FRC as a bona fida regional holding company that will hold a minimum of two active subsidiaries to be overseen and supervised by employees of the Mauritius FRC. Such a scenario could conceivably be achieved by reorganising the shareholding pattern of existing regional companies, and not necessarily through new investment transactions.

The Regional HQ strategy exemption appears to provide a strategic pathway for a new Mauritius FRC to satisfy the Main Business Test and be approved as a “Passive Income Entity”, with the benefit that only certain passive income of the Mauritius FRC (certain dividends, certain interest income, certain capital gains, etc.) will be subject to aggregation in the Japanese parent company’s taxable income and subject to Japanese effective tax rates. The active business profits of the Mauritius FRC will not be subject to aggregation.

The Regional HQ strategy exemption may be a useful option to explore for Japanese companies active in Africa and presently considering Mauritius as a potential regional investment hub.

Notes

-

Disclaimer: This blog post is intended to shed some light on the complex Japanese CFC / Anti-Tax Haven rules for Japanese companies with foreign related companies in low-tax jurisdictions, such as Mauritius. This blog post is neither intended to provide a tax opinion nor to constitute tax advice. We do not warrant that the information in this blog gives a complete or an accurate description of the J-CFC / Anti-Tax Haven rules in force and how they may be applied. Japanese companies considering the establishment of a foreign related company in Mauritius must consult qualified tax experts in Japan for case-specific advice.